Queensland has the world’s highest coal royalties

The facts, the impact and what needs to change

Coal royalties help fund schools, hospitals, roads, emergency services and other essential infrastructure across Queensland. They are also one of the ways Queenslanders benefit from the state’s natural resources.

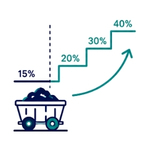

In 2022, Queensland increased its coal royalty rates during a period of record coal prices, lifting the maximum rate from 15% to 40% and making Queensland the highest coal royalty jurisdiction in the world.

Four years later, conditions have changed significantly. Coal prices have fallen, operating costs have risen and competition for investment has intensified, yet the royalty settings introduced in 2022 remain unchanged.

QRC is calling for a review of current coal royalty settings to ensure Queensland continues to receive a fair return from its resources while remaining competitive enough to support jobs, regional communities, investment and future royalty revenue.

Explore the issue

Understanding royalties

Royalties are payments made to the Queensland Government for the right to mine Queensland-owned resources.

They are paid on top of company tax, payroll tax, land tax and council rates and are paid regardless of whether a project or company is profitable or not.

Royalty revenues help fund essential public services and infrastructure including hospitals, schools, roads and transport.

What’s changed

For more than a decade, Queensland’s coal royalty system was relatively stable, with a maximum rate of 15%.

That changed on 1 July 2022, when three new royalty tiers of 20%, 30% and 40% were introduced during a period of record coal prices. The changes significantly increased the share of revenue collected by the state and delivered record royalty returns for Queenslanders.

Since then, however, the operating environment has changed considerably.

Coal prices have fallen substantially from their 2022 peaks. Operating costs have increased by 29%, while producers face higher diesel, energy and water costs, exchange-rate pressures and increasing competition from other jurisdictions seeking investment.

Despite these changes, Queensland’s royalty settings have not been reviewed.

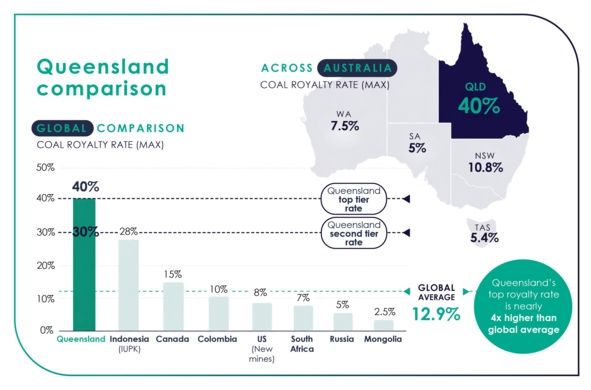

Today, Queensland’s top royalty rate of 40% remains the highest in the world, continuing to apply in a market that looks very different to the one in which it was introduced.

How Queensland compares

The state’s maximum coal royalty rate of 40% is nearly four times the global average of 12.9%.

Even Queensland’s second-highest tier of 30% exceeds the maximum royalty rate applied by every other major coal-producing jurisdiction.

Why this matters

Coal remains one of Queensland’s most important industries.

It supports jobs, businesses, regional communities and public revenue across the state, while generating billions of dollars in royalties to help fund essential services.

In 2024–25 alone, Queensland’s coal sector:

generated for Queenslanders through coal royalties over the last 10 years (to 24-25)

The discussion about royalties is ultimately about how Queensland can continue to receive these benefits into the future.

The impacts already being felt

Since the royalty changes were introduced in 2022, the operating environment for Queensland’s coal industry has changed considerably. The royalty settings have not.

Industry data and independent analysis indicate the impacts are already being felt:

gone from the sector

The coal sector shrank by $9.6 billion in 2024-25.

coal jobs lost

Coal employment fell 24% between 2022 and May 2025.

gone from local economies

Spending in regional areas where coal is a major contributor fell by $3.2 billion in 2024-25.

higher operating costs

Operating costs are up 29% since 2022, excluding this year’s diesel price increases.

Together, these figures highlight the growing pressures confronting Queensland’s coal industry as market conditions soften and costs continue to rise.

Behind every number is a Queenslander

The impacts do not stop at mine sites. They flow through regional communities, affecting contractors, transport operators, suppliers, local businesses and the families who rely on them.

Behind every statistic are real people whose livelihoods are connected to Queensland’s coal industry.

What needs to change

Queenslanders deserve a fair return from the state’s natural resources.

They also deserve a royalty system that reflects current market conditions and supports the long-term competitiveness of one of Queensland’s most important industries.

QRC is calling for a review of Queensland’s coal royalty settings.

The royalty rates introduced in 2022 were designed for a period of exceptional coal prices. Four years on, conditions have changed significantly. A review would determine whether the current settings remain appropriate for today’s operating environment and Queensland’s long-term economic future.

Any review should seek to balance four key objectives:

Maintain a fair return

Continue generating strong royalty revenue to support public services and infrastructure.

Support jobs and regions

Help sustain the industries and and regions who keep the sector strong and generate royalties for all Queenslanders.

Encourage future investment

Improve Queensland’s competitiveness when companies make long-term investment decisions.

Protect future royalty revenue

Support a competitive industry that can continue contributing over the long term.

A growing sector pays more royalties over time. A shrinking sector pays less.

Key questions answered

There is a lot of discussion about coal royalties and why a review is being proposed. Here are answers to some of the most common questions.

Why should coal royalties be reviewed now?

The current rate structure was introduced in 2022 during a period of record coal prices that were never expected to last. Conditions have changed. The policy has not.

Queensland has the highest coal royalty rates in the world, around four times the global average and nearly four times NSW’s maximum rate. Investment is allocated in a global market. When Queensland becomes less competitive, investment, jobs and future royalty revenue increasingly go elsewhere.

A review would help ensure Queensland continues to receive a fair return from its resources while remaining competitive enough to support long-term investment, jobs and economic growth.

Don’t companies already pay more when coal prices are high and less when they fall?

Royalty payments do rise and fall with coal prices. However, the six-tier rate structure itself was set in 2022 and has never been reviewed.

Since then, operating costs have risen 29%, exchange-rate movements have pushed producers into higher royalty tiers even when coal prices have not increased, and Queensland producers continue to pay more than competitors in other states at every price point.

The review being sought is of the rate structure itself — the thresholds and percentages set in 2022 — not the principle that royalties should rise and fall with coal prices.

If royalties are hurting investment, why are there still active coal mines?

Coal is a long-term industry. Mines operating today are often the result of investment decisions made many years or even decades ago.

Companies continue to make commercial decisions about existing operations, but recent activity in Queensland has largely involved the transfer of existing assets rather than significant new capital investment, new mines or new jobs.

The key question is not whether mines exist today, but whether Queensland remains competitive enough to attract future investment.

Aren’t there many factors affecting the coal sector, not just royalties?

Yes. Coal prices, exchange rates, operating costs, regulation, weather, global demand and geopolitical risks all influence the sector.

However, royalty policy is one of the few factors within government control. At a time when the industry is already facing significant cost pressures, the world’s highest coal royalty rates compound those challenges and reduce Queensland’s competitiveness.

Isn’t it fair that coal companies pay their way?

Yes. Queenslanders deserve a fair return from the state’s natural resources, and the coal sector has paid billions of dollars in royalties for decades.

The question is whether the current rate structure, introduced during record coal prices and never reviewed, remains appropriate for today’s conditions. A royalty system that drives investment elsewhere ultimately delivers less economic activity, fewer jobs and less revenue for Queensland over time.

How are Queensland’s royalty rates viewed by global investors?

Queensland’s high royalty rates and increasing cost base are affecting perceptions of the state’s competitiveness.

Many investors view Queensland as a more expensive and higher-risk destination for capital than competing jurisdictions. As investment shifts to other states and countries, Queensland risks losing future projects, jobs and economic activity.

Why review royalties if the Government has said there will be no change?

The current royalty structure was introduced in 2022 when coal prices were at record highs. Since then, coal prices have fallen, operating costs have increased significantly and producers have continued to trigger higher royalty tiers due to exchange-rate movements.

After four years of changing market conditions, a review is a sensible way to assess whether the current settings remain appropriate and whether they continue to support Queensland’s long-term competitiveness and economic future.

Looking for more detail?

Download the full Coal Royalties FAQs and Mythbusters guide.

How you can help

Understanding the issue is the first step.

If you would like to learn more or support a review of current royalty settings, there are several ways you can help.

Sign the petition

Support a review of current coal royalty settings by adding your voice to the Regions Before Royalties campaign.

Speak to your local MP or mayor

Share your views on the importance of mining jobs, regional communities, investment and long-term economic opportunities for Queensland.

Learn more and share the facts

Explore the data behind Queensland’s coal industry and royalty system. Access fact sheets and reports to better understand the industry’s contribution, current challenges and why a review of royalty settings is being proposed.

Resources and downloads

Access the Queensland Coal Royalties Fact Sheet, Coal Economic Contribution Report and explore A Little Bit of Queensland Goes A Long Way for additional information, data and analysis.